Royal Pingdom has an excellent post on the web usage (which is what they can measure) of the top OS use around the world. It’s amazing to see the difference between Africa, Asia and South America as opposed to Europe and North America.

While, as a developer, it’s a lot more sexy to work on the cutting edge operating systems like iOS and Android you’d be making a mistake to do that in Africa. Unless you’re developing apps that are global in scale or you’re doing client work, you should be focusing on Symbian (or Samsung’s Bada OS in some countries). It’s where the numbers are.

Reaching Ordinary Africans

This brings to mind something I’ve been thinking about for a while. Mxit, as most people know now, is the mobile social network out of South Africa. It was built about 4 years ago and has 20 million+ users.

Mxit didn’t get big because they tried to build something that was cool and sexy for the middle/upper classes in South Africa (which is what so many try to do there). Instead, they built one of Africa’s most successful tech companies by focusing on everyday South African youth and fulfilling their needs.

In fact, you can take this one step further. Almost any meaningful success in Africa’s mobile or web space has been from companies focused on meeting the needs of ordinary people. Go ahead, think of the success stories in Africa’s tech space, now name them and see if they’re made for a global market, Africa’s elite, or for the masses.

]]>

People are excited about M-Kesho (money for the future) which launched yesterday, where Safaricom has linked their mobile payments service Mpesa as a joint venture with Equity Bank in Kenya. This basically extends Mpesa into a bank and insurance company, with the future offer of microcredit as well.

- Equity bank has 80 branches in Kenya.

- Mpesa has 17,500 outlets in Kenya.

- There are approximatey 8.4 million bank accounts total

- Equity has about 4.5 million bank accounts

- Mpesa has 9.5 million users

- Kenya has 107,000 credit cards in circulation

See the pattern? These are are big companies with huge local connections and inroads into the popular culture. This is a strong indicator that every Kenyan will have access to banking and insurance via mobile phone very soon.

“This is a bank account introduced by both Equity and Safaricom where customers can earn interest from as little as 1 Ksh. Customers can withdraw cash from their Equity Bank Account to their Mâ€PESA accounts and customers can also deposit through their Mâ€PESA accounts to their Mâ€KESHO Bank account. Other features of the account include Micro credit facilities (emergency credit availed through Mâ€PESA), Micro insurance facilities as well as a personal accident cover that translates into a full cover after 1 year. For one to open this account, the person must be an Mâ€PESA subscriber.”

Reality Check

As others have pointed out, there have already been links between mobile payment systems like Zain’s Zap and banks like Stanchart. So, this isn’t exactly groundbreaking and new. Why is it big then? It’s big because of who is doing it: the giants of the banking and mobile sector.

Rombo has written a particularly good post about M-Kesho. She asks some hard questions, like who really benefits out of this deal: Equity or Safaricom?

It’s hard to say, but I wonder if the pressure put on by regular banks onto the regulator about how close to a bank Safaricom’s Mpesa really has forced their hand. Did they have to choose a banking partner in order to stave off the regulator, or did they do it to increase market share and positioning?

Finally, I think this move, like the moves made by Safaricom in the past on this mobile banking space are shortsighted. Yes, it gets them more subscribers and it does solidify their grip on the mobile market in Kenya, that is working. However, mobile money and payments are much bigger than just one operator or one bank. Becoming the “Visa of the mobile payments space” all over Africa (the world?), is a much bigger deal than being the biggest fish in Kenya’s small payments pond.

]]>We’re all born in a small “company town“, where the mobile operators are the landlord and the bank, the grocery store and the mafia.

Interestingly enough, there is a completely different industry built on a much more open standard that separates infrastructure from content, transactions and use. That is, the internet. So, as we get closer to a world where there is less of a difference between the mobile and web worlds, then we see what happens when a strangling monopoly won’t give in to an open system. The open system bypasses it.

Some examples

Multimedia

It starts getting humorous when you start looking at value-added services like location, video or images. I sat there and listened to the mobile operators talk about how “MMS will never be the equivalent of SMS” – their cash cow. Of course, not with them running it.

However, 2 days later we see this headline from YouTube, “just since last Friday, when the iPhone 3GS came out, uploads increased by 400% a day.” What? Yes, that’s a staggering number and it’s due to the fact that no operator is running it, they’re just selling the underlying data structure.

Messaging

Twitter is a great service that allows personal networks to form and SMS messaging to take place on an ever extending one-to-many and many-to-many basis. It also works on the web, in fact, that’s one of it’s great strengths – the ability to treat any channel as native. When I look at Twitter, which is 3 years old now, I have to wonder why we still don’t see a Twitter-clone offered up by any of the operators working in the 192 countries that Twitter isn’t in. For goodness sake, the only major cost for Twitter is the “to-many” part of it, and that’s virtually free to an operator on their own network.

Location based services

When the mobile operators of the world wanted to control their location services, in the early 2000s they kept their prices too high for large and small consumer-facing organizations to buy their services. So, the web went around them… The entrepreneurs saw an advantage to going out and getting the number off of every mobile phone tower and doing basic triangulation from them and WiFi signals. Voila, the operator is bypassed and now makes no revenue off of a service that it could have provided for a lower fee.

Operators can’t build real consumer services

I’ve heard a a number of comments from within the industry like this:

“we’ve had the ability to do such-and-such (insert your favorite third-party service here) for a long time, there’s nothing special about YouTube/Twitter/Apple doing this.”

This is a true statement (most of the time), so why are there millions clamoring for these other services and not the ones that the operators offer?

The release of increasingly more user-friendly phones, coupled with services that bypass the traditional restrictions placed upon everyone by the operators, has created a way for the internet players to replicate or make irrelevant many of these same services offered by the operators. This will continue to be the pattern too, as the two industries collide.

What the operators should do is open up their basic infrastructure for third-parties to build consumer-facing applications on. Take a smaller cut on each application or service, and create a true ecosystem that supports more developers and companies trying to figure out ways to make more money off of your framework.

]]>

]]>“Steve Vosloo noted that m-learning summits have two main goals: To introduce and popularize the mobile phone as a tool for engaging students, and secondly, to identify local content needs. Examples of this may include applications that support grade submissions and attendance in remote locations or projects that explore how texting can be used in literacy.”

The Global Messaging Congress is underway in London. I’m here to speak about extending the power of messaging – providing critical information in disaster zones. My goal is to showcase some of the interesting solutions we’ve seen in this space, from Ushahidi to Cartagen to SMS GeoChat – among others. I’ll also be calling upon the experts here to think of what they would do with their knowledge and expertise with the tools that they know and understand so well if called upon to do so during an emergency.

The Global Messaging Congress is underway in London. I’m here to speak about extending the power of messaging – providing critical information in disaster zones. My goal is to showcase some of the interesting solutions we’ve seen in this space, from Ushahidi to Cartagen to SMS GeoChat – among others. I’ll also be calling upon the experts here to think of what they would do with their knowledge and expertise with the tools that they know and understand so well if called upon to do so during an emergency.

Notes from the Opening Remarks

It’s time to reinvent the industry. The personalization market is dying – the days of big money in ring tones and wallpaper is over. The economic crisis is tough and the regulatory market is not benign. So, why be optimistic?

1. Applications. Apple’s iPhone has changed the customers view of what an application is. The fact that a farting application can make $800,000 sends a certain signal. The question is how does this model change things once it moves beyond the early adopters?

2. Mobile social networking has become the epicenter of innovation. New business models and money making opportunities are being thrown off by this new market.

Operators, especially in places like the US, are trying to control what content shows up on the network. The government regulators and the operators policies are out of control, in fact there are some cases where the industry is suiting on the behalf of the customer. This will cause a downsizing in the US market for the next couple years from the content providers.

Keys to succeeding in the mobile social networking space:

- Alternate billing solutions. You have to have your virtual currencies tradeable on the social networking platforms. All payment methods must be accepted, from SMS payments to credit cards.

- Content. You have to have something there for people to use, read, play with. Quiz applications are the big thing right now (brings up example of a quiz app being #3 on iPhone apps right now).

- Discoverability. The main problem from users perspective has been trying to find the applications and content that they want. This is an issue for both the content providers and the operators to solve.

Role of the operator is changing, it specifically has a large impact in billing. They need to take a significant cut in the amount they charge for this service – 50% is just ridiculous, it must change as it’s not sustainable or excusable.

“Apple’s app store is the big shadow hanging over all of us, except of course that they’re never here…”

]]>

Some takeaways:

- Lower levels of ICT access and usage in Africa can be attributed to weak telecommunications infrastructure, generally low economic activity, irregular electricity and a lack of human resources.

- Income and education vastly enhances mobile adoption (over gender, age or social networks).

- Mobile expenditure is inelastic, meaning higher income individuals spend a smaller proportion of their income.

Charts

There are a number of interesting charts within the paper. One of which shows the elasticity of usage depending upon income (top 25% of the population vs bottom 75%).

Personally, I was fascinated to see a study on the average expected cost of a mobile handset.

I’ve got a PDF version of the report here. Like this conference, it’s mired in academic language, but it’s an incredibly informative and useful report if you can get past that:

ResearchICTAfrica Report – ICTD 2009 [PDF]

(sidenote: the academics here at this conference could use a course in communications, it’s often difficult to decipher what they’re actually trying to say…).

]]>A uniquely African solution to an African problem

iYam is a simple mobile phone-based mobile phone directory (Fritz calls it a “mobile mobile phone directory”). It is a way to lookup businesses, service providers and contacts from your mobile phone.

iYam is a simple mobile phone-based mobile phone directory (Fritz calls it a “mobile mobile phone directory”). It is a way to lookup businesses, service providers and contacts from your mobile phone.

That doesn’t sound very exciting, and it shouldn’t if you live anywhere outside of Africa. However, those of you in Africa will recognize immediately why this is such a valuable service. You see, most countries in Africa don’t have a mobile phone directory for finding goods, services or individuals. There is no easy way to contact most businesses in Africa. It provides a simple, accessible solution to the problem using the ubiquitous SMS protocol.

Example uses:

- Looking for computer dealers to buy your next laptop? iYam will give you their contact numbers.

- Looking for software developers to help you work on your project? iYam will give you some contact numbers.

- Has your phone just been stolen and you want to get back some of your old contacts ? Find their numbers using iYam.

- Someone just called you but you seem to not remember who has that phone number ? iYam can tell you a lot more about the owner of that number.

iYam is ground breaking because it is a new form of search. Instead of searching for web pages, you search for people. You are only allowed to use 155 characters to describe yourself as you add yourself to the direcgtory, forcing a certain amount of constraint.

“The way we develop here in Africa will be different from the way the big nations developed. They grew up with computers. We are growing up with mobile phones.

– Fritz Ekwoge”

Business cases and investment opportunities

Most of the discussion between Fritz and I revolved around the business case for his product, and the investment money needed to make it a real business. As always, the Achilles heel for any smart, entrepreneurial programmer in Africa is how to get enough money to work on something beyond the idea and prototype phase.

-

Business Models

Plan A: Strike deals with local Telecom operators to charge a small extra fee for each SMS passing through our service.

Plan B: iYam only displays the first five results per SMS request. As the service gets more popular, many businesses will be eyeing for the top position. They will have to pay for that.

Advantages

Hardware requirements are modest. Currently, in it’s alpha stage, iYam is powered by a laptop plus two mobile phones. These will be replaced with a bigger server and some GSM modems as traffic increases. To reduce international communication costs, the iYam setup can easily be replicated in other target countries.

Disadvantages

SMS will definitely cost a lot as the service becomes more popular. But revenue should cover those costs, or deals could be made with telecommunication companies to reduce our SMS costs.

Growth

The market in Cameroon alone is sizable, but there is no reason that once this moves from prototype to service, that it can’t be replicated in other African markets.

Technical Details

Currently, it does not work with the local CDMA provider CAMTEL, because they don’t exchange SMS with the GSM providers. However, it does work with other countries, as Ghana and Gabon have already been tested.

Final thoughts

As I mentioned in the beginning, I’m enthused by both Fritz and by iYam. Of the two, I’m more excited by Fritz, because it’s easy to come up with ideas, and hard to execute on them. This is his second time to have done just that. This is the perfect opportunity for an early-stage investor to get involved and help scale an idea and prototype to a real product making real money.

]]>The basic premise is that we cannot expect great innovation and technological breakthroughs from Africans until computers are ubiquitous in Africa. He states that the mobile phone just doesn’t provide the platform necessary for real programming and hacking to happen. That mobile phones are an interim step, not the final answer. And finally, that IT infiltrates social groups when, and as, they find a personal need for it.

Mobiles vs PCs

Cory’s points are valid. All things being equal the best device to get into the hands of kids is a personal computer. Having a full-sized keyboard and monitor are better than trying to program on a mobile phone. There’s nothing to disagree with there.

One of the reasons I have liked the OLPC initiative is because they have forced the door open to low-cost laptops in the developing world. The more computers we get into the hands of kids, the better Africa’s future will be.

However, there’s the reality that I see on the ground as I travel. Sure, there are a few people with access to computers and who are creating applications and services through it for the web, PCs and mobile phones. They generally have a college-level education and are entrepreneurial in nature. A lot of the innovative work being done on the PC is applications for the mobile phone.

So, PC access plus education tend to equal more mobile applications.

The other item that I’m finding more and more of a problem for mobile developers is getting the license to actually get their product to market, much less sell it. If they do, it’s at outrageous rates that the carriers should be ashamed of.

Merging mobile phones, PCs and the web

Here’s an interesting question. What happens as we see the merging of mobile phones, PCs and the web? We’re talking about the “mobile web” more and more, and how smarter devices like the iPhone, Android and Symbian devices let us do almost as much as we can on a PC.

Will full-sized PC computers become less relevant as we simply attach keyboards and/or monitors to the device in our pocket?

That’s a question I’d like to explore more. Are there examples of this type of work happening already in any organized fashion?

[Update: I see that MobileActive and Steve Song have weighed in on this as well.]

]]>

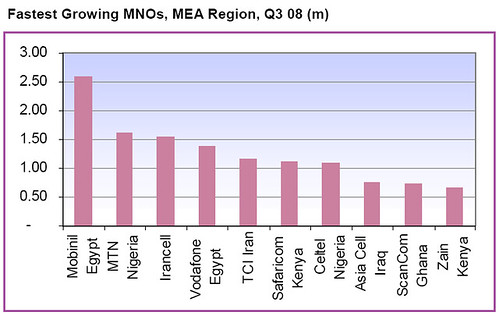

“Mobinil in Egypt produced by far the best result in the region, with 2.58m net adds – more than it connected in the first two quarters of the year and nearly one million more than second placed MTN Nigeria managed. The Egyptian market has been booming since the launch of the countryâ€

s third network, but as is so often the way, the incumbents have been the main beneficiaries.”

Nigeria has had absolutely amazing growth numbers in mobile phone subscribers, and even though they’re one of the top in this report, they still can’t beat their Q2 2008 quarter when they added 7,380,000 connections (yes, that many in one quarter). That is more than double what any other carrier has been able to grow their connections by in any other African country.

“Kenyan companies take sixth and tenth. Safaricom, the Vodafone associate, added 1.12m new connections in the quarter to strengthen its lead over Zain Kenya. Zain remains the main threat in Kenya, but its 0.65m net adds in Q3 do not fully offset the loss of 0.98m seen in Q4 07 and Q1 08 and the companyâ€

Overall, we’re seeing a slight decrease in growth in Africa as a whole. Not much, not even near a plateau, but lower growth rates than in previous years. There are still many more fat bottom lines ahead for these carriers, but they do have to start thinking a lot more about two big areas: data and customer service.

]]>

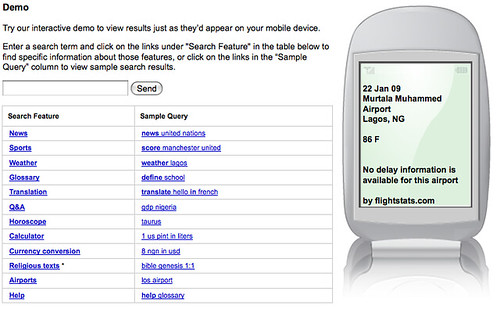

After a quick check with someone at Google Kenya, I verified that these are the only two African countries that Google has released SMS search in at this point. It seems that this would be quite simple for Google to turn on in almost every country in Africa, so I wonder if one of the bottlenecks is actually getting the specific shortcode that they want (4664 or “GOOG”).

Though it’s hit or miss on some of the queries right now, at least it was as I tested it through the web interface, it’s still a valuable service that I hope the make available in more countries soon. They’re following the basic rules for technology in Africa, which is to design for the lowest common denominator: SMS-only mobile phones.

]]>