Get the full 2.5Mb download of the report here: (ON Africa Report).

The gaps they see are familiar to many. We all know that part of the problem is the education system isn’t setup for problem solving, it’s about rote learning.

“Students are not afforded clear paths for cultivating competencies related to practical thinking and creative problem-solving—skills needed to successfully build and manage a business.”

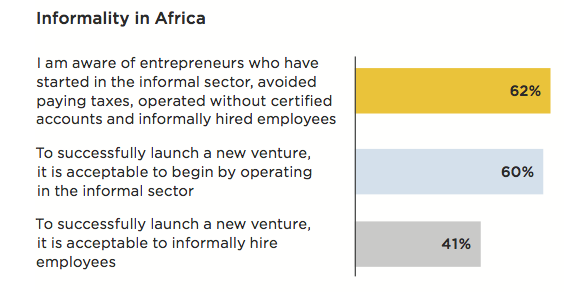

African entrepreneurs aren’t helped by government policies and regulations, in fact they’re better served by doing it informally first, as seen in the responses on this to the question:

African entrepreneurs prefer starting off informally

Another great quote about the cultural pressure not to do a startup:

“Parents and guardians pressure their wards into studying more professional courses rather than entrepreneurial or creative ones, sometimes even tagging them as ‘crazy’ when students make the decision to work in start-up companies or develop their own businesses.”

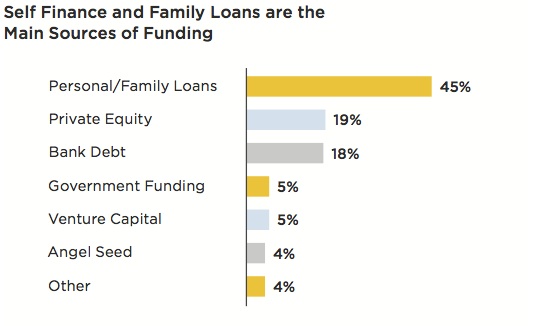

There’s also a gap in where companies find seed funding:

The survey focused on four areas of the entrepreneurial environment:

- Entrepreneurship assets: Financing, skills and talent, and infrastructure

- Business support: Government programs and incubation.

- Policy accelerators: Legislation and administrative burdens.

- Motivations and mindset: Legitimacy, attitudes, and culture.

There are a lot of recommendations for each of these four areas that the report covers, enough for anyone running a tech hub, incubator, university and especially the government to think through.

]]>m:lab East Africa after 2 years

The study which was conducted between April and May 2013 focused on 3 key activity areas at the m:lab namely:

- Mobile entrepreneurship training

- Pivot East regional pitching competition

- The incubation program

The highlights are found on the iHub blog for now, the full report to be downloadable as soon as it is formatted.

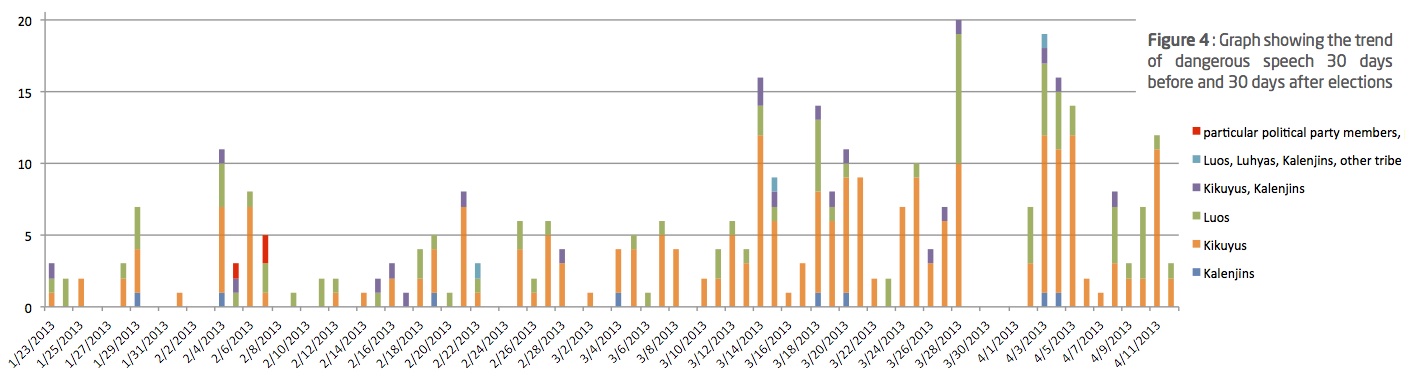

Umati: monitoring dangerous speech in Kenya

The Umati project sought to identify and understand the use of dangerous speech in the Kenyan online space in the run-up to the Kenya general elections. Apart from monitoring online content in English, a unique aspect of the Umati project was its focus on locally spoken vernacular language; online blogs, groups, pages and forums in Kikuyu, Luhya, Kalenjin, Luo, Kiswahili, Sheng/Slang and Somali were monitored.

No organization is in a better position than the GSMA to get data on mobiles globally. After all, they’re the global association for almost all of the world’s mobile operators. When they release a report, it’s worth looking at. This time they’ve done a great job of putting some of their research and statistics into visuals, check the full report on “The Mobile Economy 2013” website. It’s a virtual treasure trove of valuable global and regional mobile information.

Some interesting takeaways:

- 3.2 billion mobile subscribers at the end of 2012

- Data is what is driving the growth to the tune of 1,577 Petabytes of data, with the biggest driver being video.

- Africa is expected to see a 79% growth in data by 2017

- SMS usage is growing, but slowing in growth to 28%. This is thought to be from VOIP and social networking apps.

- 77% of all connections globally are pre-paid

- The GSMA is pushing their “OneAPI” approach, which I wish the African operators would subscribe to, as everyone would make more money – MNOs included

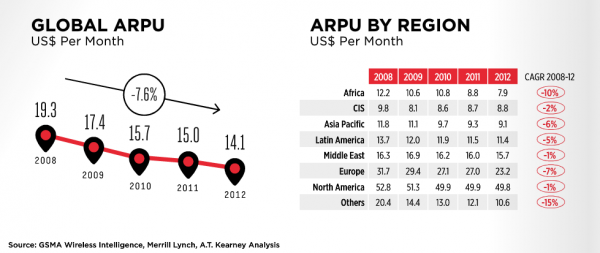

- Average revenue per user has dropped form $30.3/month in 2008 to $25.9 in 2012 – this is a big deal in Africa.

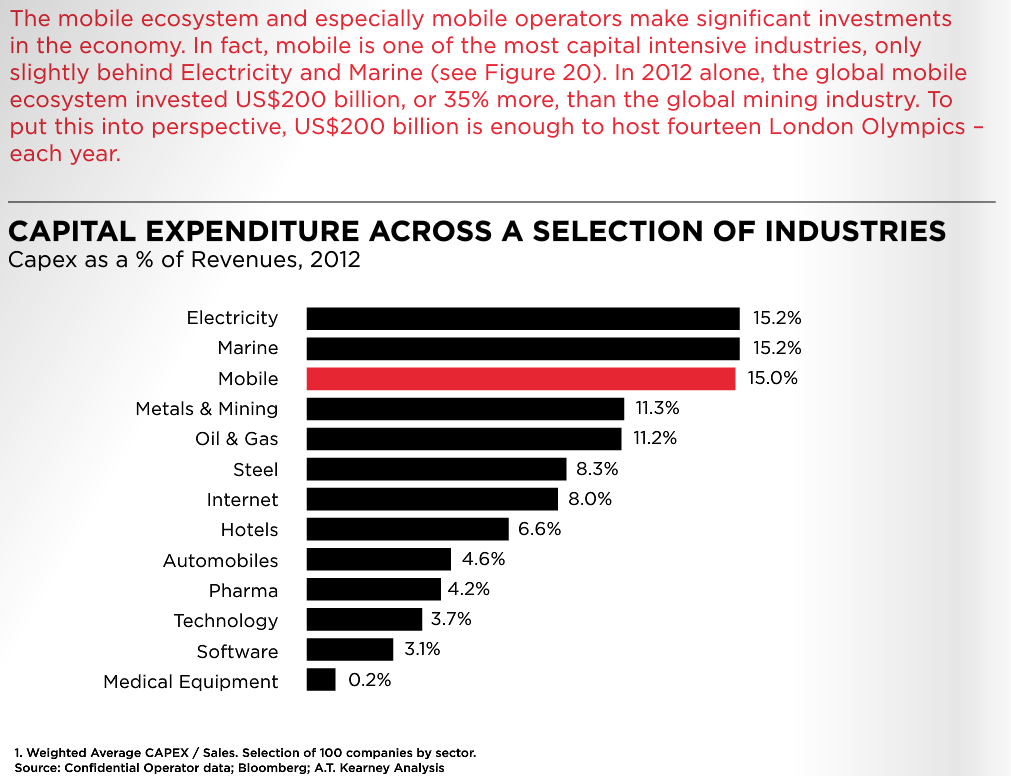

Most people don’t appreciate just how much investment goes into creating viable mobile networks. To put that in perspective, see the chart and comments below:

The mobile industry, if you go by this GSMA report, are all about personal security and privacy. We know this is a load of crap, but we can all pretend that the mobile operators really are acting in our own best interests… They are a long way from their mantra of, “an industry supporting and protecting citizens”.

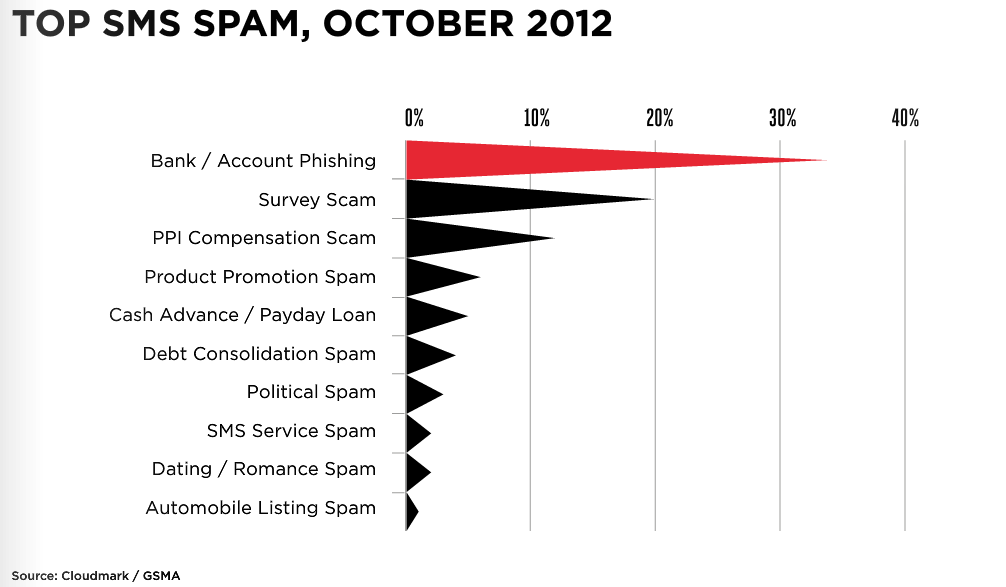

Top SMS spam categories:

Few organizations do as good of a job as Praekelt in creating well-designed applications that are used by millions of people in the continent. A couple times a year, they take that same level of quality and create new videos and resources to better showcase Africa’s tech statistics. Here’s their newest video.

Game Creators: an Interview of Maliyo Games in Nigeria

Good interview of Maliyo Games founder and the opportunity in Africa’s gaming space.

Why do you think the African audience is looking for African games instead of Farmville or Mafia Wars?

“Itâ€

s not so much what they are looking for, more what is being pushed to them. Our games ‘Okada Rideâ€

Check out Maliyo’s website to get their games.

Opera’s “State of the Mobile Web” for Africa 2012

Opera puts together a great resource of user-based statistics [PDF link]. It’s a country-by-country breakdown of mobile penetration, user growth, top domains and top handsets used. Here are a few of the interesting tidbits:

Opera puts together a great resource of user-based statistics [PDF link]. It’s a country-by-country breakdown of mobile penetration, user growth, top domains and top handsets used. Here are a few of the interesting tidbits:

- Across Africa, data growth seems to outpace page-view growth. This fact suggests that Africans are browsing larger pages and most likely, using richer, more advanced websites.

- Facebook is the top domain in every country except for these six, where Google leads: Egypt, Guinea, Djibouti, Comoros, Central African Republic, and Algeria.

Mobile Reporting Field Guide

UC Berkeley has created a mobile reporting field guide, useful for people doing data collection and research as well as activist types.

Upcoming Tech Events in 2012

PyCon South Africa – Cape Town, Oct 4-5

DEMO Africa – Nairobi, Oct 24-26

Tech4Africa – Joburg, Oct 31-Nov 1

AfricaCom – Cape Town, Nov 13-15

Mobile Web Africa – Joburg, Nov 28-29

(If you know of other tech events coming up before the end of the year that you think belong here, put it in the comments and I’ll add it later.)

Some Self-Serving Links:

- My BBC article on Africa’s tech hub growth

- Ushahidi v2.5 “Cairo” launched yesterday, really big upgrades and fixes here.

- We’ve open sourced the SwiftRiver code base, thanks to @69mb, @bytebandit and @brosage for the hard work.

- I’m excited that we’re having a Fireside Chat with Isis Nyong’o, MD Africa of InMobi, at the iHub on Aug 16.

- Keep an eye on the iHub Blog as it’s really coming alive with new stories from around the Kenyan tech community.

The position and reason for this paper is best summarized below.

“The success story of mobiles in the developing world is well known. Yet in the case of extending data services in emerging markets, there is a real danger of some serious policy mistakes. As in developed markets, broadband strategies in developing countries have tended to focus on investment in fibre. This is too simplistic. This focus on fibre may miss an opportunity for a transformational change built on the capabilities and in particular accessibility of mobile broadband. The early evidence suggests that mobile internet is spreading as quickly, in some developing countries, as mobile telephony did originally.”

Traditional definitions of broadband have a narrow focus on bandwidth and speed. This paper uses a wider definition, as broadband policy needs to consider the entire ‘eco-system†of internet and data services from both a demand and supply-side perspective.

Content Sections

- Mobile Internet usage and demand in Kenya: The experience of early adopters (David Souter)

- The potential of mobile web content in East Africa (Erik Hersman)

- Spectrum policy and competition in mobile services (Thomas W. Hazlett)

- Rethinking mobile regulation for the data age (Martin Cave & Windfred Mfuh)

- Building next generation bradband networks in emerging markets (Luk van Hooft)

The Diffusion of the Mobile Web Across East Africa

Mobile web content is growing at an astounding rate. It rose 2.6-fold in 2010, nearly tripling for the third year in a row. Official Kenyan industry statistics show that mobile internet subscribers will grow by approximately 843% for the 12 months to September 2011.

What I like about papers like this is that I get to use words that normal people don’t use. I make a case for international content and platforms as “drivers of diffusion” of data across East Africa. That simply means that these platforms and content are helping to spread the use of data more deeply into the region, and allowing local players to get in at lower costs.

International web content is by far the most widely available and used in East Africa. This is in large part due to the ease of finding and disseminating this content, as well as its normalized licensing schemes and reliability. International platforms also carry a majority of the content that is currently being viewed on mobile phones. The following are the types of content that are most important to consumers in East Africa, according to our interviewees:

International web content is by far the most widely available and used in East Africa. This is in large part due to the ease of finding and disseminating this content, as well as its normalized licensing schemes and reliability. International platforms also carry a majority of the content that is currently being viewed on mobile phones. The following are the types of content that are most important to consumers in East Africa, according to our interviewees:

- International entertainment news (sports, gossip, lifestyle)

- Local news

- Breaking news

- Facebook (and to a lesser extent other social network tools such as Mig33, Mxit and Twitter)

- Jobs

- Dating (chat and relationships)

- Religion

- Local video/media

The reasons are that international platforms, such as Facebook, Yahoo!, BBC, CNN, Google and Wikipedia, have already been tailored to work on the most widely used data- enabled handsets. This contrasts with local content providers, many of whom have yet to tailor their websites for mobile access. In addition, local content less available at present, not as easy to license, and often cannot be reliably guaranteed as a long-term source.

Local Content

I interviewed a number of executives from Kenya, Uganda and Tanzania. There was a clear belief that while international content, increasingly localized for the market, is currently king, local content has the greatest growth potential because it is more highly valued by consumers.

While local content developers lack scale they have advantages that the global platforms do not. For one, they understand the local tastes and culture so customers value their content more. The consumer benefits of truly local content and platforms could be large.

The Government Role

There is still a lack of concrete government policies for government services or content to be made available or accessible via the mobile in any country in East Africa, even though this is the primary channel by which citizens could access services online. There is a solid case to be made for mGovernment, instead of just eGovernment.

To underline this, the most popular Kenyan Government website (Kenyan Revenue Authority) is shown as seen on a PC screen, a smartphone (HTC Desire) and a typical 2G internet enabled handset (Vodafone 350). The website is most clear and easily accessible via a PC interface (and consumer interaction primarily is through downloadable pdf files). There are no browsing problems when accessing through a PC-based browser. The KRA website is also accessible via the native Android browser in the HTC Desire Smartphone. The HTC Desire also allows downloading and viewing of pdf files. However, the native browser on the Vodafone 350 (a basic 2G EDGE handset) does not present the KRA website in a usable format. As can be seen, the website is badly rendered and quite impossible to navigate.

Possible government services to be made available via mobile web:

- Paying bills

- Service delivery questions and concerns

- Taxes – access, information and filing

- Health – access or appointments, information

- Public job search

An argument can be made that m-government services would have a greater impact if the focus were on supplying tools for small businesses to interact with government, rather than only making services available for citizens in general. By removing the barriers to entry for small businesses, the government would be providing a service that increased usage, decreased business costs and had a potential tax revenue increasing effect due to filing and paying on time.

Summary

East Africans are accessing the web primarily through their mobile phones. The new medium is enticing them online with the new services and content provided through a new medium. Broadband penetration rates are low enough in this region that we are not yet seeing the displacement of newspapers, radio and TV seen in other, more connected regions of the world. However, as with all network technologies, there is the potential for reaching a tipping point. This will depend on the provision of enough mobile web content that is valued by East African consumers.

The content driving East African users online is currently largely provided by international news and content sources, such as Yahoo! and the BBC, and also by global internet platforms, such as Facebook and Googleâ€s Gmail. Even taking into account the decreasing data costs, falling data-enabled handset costs, and the increased availability of broadband, there would not be enough traction locally to get to the critical point if the content were not available.

These international content sources and global web platforms generate demand, and therefore allow the mobile network operators to decrease costs as more users come online. International content is thus providing a pathway for local content creators. While local content is in high demand and there is a rapidly increasing user base, the mobile web content space in East Africa is in its early stages, and there are no

clear leading content providers. At present the key trend is the provision of increasingly localized content by the leading global companies.

This paper has identified two important barriers to the further diffusion of mobile internet usage across East Africa: lack of m-government policies; and, more important, an absence of charging mechanisms which share the cost of mobile internet access between end-users and content providers. If governments embraced mobile-based provision of services and provided access free of usage charges to end-users (sharing the efficiency gains through payments to network operators), the potential impact on internet access could be dramatic. The challenge for governments and local developers of mobile web content is to utilize their local cultural understanding and ability to maneuver quickly to make their content more relevant and affordable to end-users.

(Note: This is summary of my section. Download the full 2Mb PDF report to read the section in its entirety, and to read the other 4 sections of the paper.)

]]>

A new report shows that Africa has 12% of the new mobile subscribers in the world, adding 20.1 million in Q1 2010. That’s a sizable amount. What’s actually more interesting to me is that they’re saying that the continent now has 47% penetration, which means that there’s a lot of growth yet to be had as compared to the rest of the world.

[One of these days I’ll have the £400 to purchase and really dig into these reports…]

Street hackers and the Neighbourhood App Store

Jan Chipchase gives us some background on how the mobile phone street-hacker culture originates:

“I like to think of it as a neighbourhood app store – and in many ways itâ€

Nokia battles the Chinese

As David put it, “Nokia lost the high end to iPhone/Android/Blackberry, now battling China’s cheap phones on the low end. Things not looking good.” (link)

]]>“For instance, it sold 432 million devices in 2009, or more than its top three competitors combined, however, its average selling price for all models has plummeted 44 percent in the past five years to 62 euros.”

A decade of ICT penetration in Africa

“By the end of 2008, Africa had 246 million mobile subscriptions and mobile penetration has risen from just five per cent in 2003 to well over 30 per cent today. The high ratio of mobile cellular subscriptions to fixed telephone lines and the high mobile cellular growth rate suggest that Africa has taken the lead in the shift from fixed to mobile telephony, a trend that can be observed worldwide. The number of Internet users has also grown faster than in other regions.”

Despite this growth rate, penetration is far below the rest of the world. As the report states, “Less than 5% of Africans use the Internet, and fixed and mobile broadband penetration levels are negligible.” The global average is 23% internet penetration. This is due mainly to cost, but also to coverage over a very large continent that lacks population density outside of major cities.

Not all of Africa is created equal

If you’re a company trying to make money off of providing services or products to mobile phone users in Africa, you have to think strategically. You can see from the chart below that the countries you should focus on first are Nigeria, South Africa, Kenya, Ghana, Tanzania and Côte dâ€Ivoire.

This holds true for the internet as well. You’ll note that many of the top countries for mobile penetration are also countries with a strong internet growth rate.

“According to a recent household survey conducted by Research ICT Africa, the main location of Internet use in such countries as Benin, Burkina Faso, Cameroon, Côte dâ€Ivoire, Ethiopia, Ghana, Kenya, Nigeria, Rwanda, Senegal, Tanzania and Zambia is the cyber/Internet café.”

Leapfrogging… with a catch

Many reports you read will sing the praises of the mobile networks and how the leapfrogging of landlines has helped Africa. That’s true, and I’m one of those people. However, it comes with a catch, and that catch is that the lack of landlines in Africa means that it’s a lot harder to get fixed-line broadband penetration, whether ADSL or otherwise. This keeps prices high and primarily availability is only in urban areas.

This gives the mobile operators a significant advantage in Africa, and it’s the reason why 3G (mobile broadband) technology is leading the way and why most of the growth will be through the mobile networks.

To put it in real numbers. By the end of 2008 there were only 635,000 fixed-line broadband subscribers in all of Africa, representing 0.1% of the population, whereas the world average is 6%. Mobile broadband sees 7 million subscribers with a penetration representing 0.9% of the population, again 6% being the global average.

In Summary

This report is an absolute gold mine of valuable data on internet and mobile phone usage, penetration and growth rates in Africa. I could go on with more graphs and thoughts on each section, but you should do yourself a favor and download the free copy and read it.

Finally, some last charts showing mobile cellular subscriptions, mobile broadband and internet subscriptions by country in Africa:

Blycroft does an excellent job of aggregating data on African mobile phone markets each quarter. They’ve compiled their report for Q2 2009 which includes subscriber numbers and other useful data, titled “The Africa and Middle East Mobile Telecoms Market in Figures 2Q 2009“. The mobile data includes GSM and CDMA networks, but excludes fixed and CDMA-wireless networks, which are classed as an extension of the fixed network. Make sure you get over to their site and pickup the full report, available for £399.

Blycroft does an excellent job of aggregating data on African mobile phone markets each quarter. They’ve compiled their report for Q2 2009 which includes subscriber numbers and other useful data, titled “The Africa and Middle East Mobile Telecoms Market in Figures 2Q 2009“. The mobile data includes GSM and CDMA networks, but excludes fixed and CDMA-wireless networks, which are classed as an extension of the fixed network. Make sure you get over to their site and pickup the full report, available for £399.

Mobile subscriber growth numbers by African region:

comparing Q1 to Q2 2009

Statistics for the North Africa region for 2Q 2009 cover 6 states and 131,109,223 subscribers, up from 123,903,195 in 1Q 2009, and representing a net gain of 7,206,028 ( 5.8 percent)

Statistics for East Africa cover 12 states and 61,983,813 subscribers, up from 58,257,266 in the previous quarter – an increase of 6 percent. Year- on-year growth saw some additional 18,382,201 mobile subscribers in the region; a growth of 42 percent.

Statistics for South Africa cover 10 states and 62,175,521 subscribers, up from 60,093,764 in the previous quarter – an increase of about 3.5%

Statistics for West Africa cover 16 states and 125,616,329 subscribers, up from 118,644,669 in 4Q 2008 – an increase of approximately 6%.

Statistics for Central Africa covers 11 states, and 34,125,739 subscribers. (Note: I’m missing the Q1 2009 numbers for Central Africa, if you have them, please pass them on so I can update the chart)

Top 20 African States by Mobile Penetration

There’s not much available in the non-pay version to see, in fact, they’ve removed almost every meaningful number and graph. However, there is one graphic covering the top 20 African states by mobile penetration.

As usual, South Africa and Egypt show large subscriber numbers, both at around 50 million users. Interestingly, penetration in South Africa is over 100%, but is still only at 60% in Egypt, meaning there will be much more growth there than South Africa in the future.

When discussing penetration rates, we always see a higher proportion of small and island countries due to the fact that it takes a lot less mobile users to have a significant percentage covered. Unfortunately, that’s somewhat meaningless in a chart like this, because they’re mixing small with large countries. More useful would be two charts that are separated on population levels.

]]>

Africa Telcom News has released a free report, called the African Mobile Factbook, that gives all of the major numbers on subscribers, penetration rates, profitability and growth potential for every African carrier and country. As anyone who is tries to do research in this space knows, it can be difficult to get some of these mobile phone statistics for Africa, so this is a welcome source for information.

Interesting Facts

- Nigeria, South Africa and Egypt are the fastest growing markets

- Africa has become the fastest growing mobile market in the world with mobile penetration in the region ranging from 100% to 30%

- Pre-paid subscriptions account for nearly 95 percent of total mobile subscriptions in the region

- Most of the mobile operators are home-grown. In 2005, the continentâ€s seven largest investors controlled 53% of the African mobile market

- Across most of Africa, SMS is likely to be the only non-voice value-added service to gain mass market popularity in the immediate future

- East Africans pay taxes of between 25% and 30% on mobile phone services, compared with an average of 17% across Africa

- African states with less than 600,000 subscribers and includes Burundi, Cape Verde, Central African Republic, Comoros (Union of the), Djibouti, Equitorial Guinea, Eritrea, Gambia (The), Lesotho, Liberia, Mayotte, Sao Tome and Principe, Seychelles, Somalia, Swaziland and Rwanda.

Subscriber Numbers and Penetration Rates

At the end of 2007 there were 280.7 million mobile phone subscribers in Africa, representing a penetration rate of 30.4%. The chart below shows the historical numbers up until 2007, with projected growth and penetration rates through 2012.

Even more interesting, when you look at the major African markets, is to see the huge growth potential for areas that are already very profitable. As can be seen Nigeria, Kenya and Egypt have the greatest growth potential.

Africa’s Mobile Phone Operators (carriers)

There are (or will be) a staggering 11 mobile phone operators in Nigeria, with 4 in Kenya and South Africa, and 3 in egypt and Morocco.

“MTN dominates the African market with over 73.9 million subscribers in the region as of 4Q 2007 followed by Vodacom (33.4 million), Orascom (32.4 million), Zain (30.6 million) and Orange (27.7 million), respectively.”

Size doesn’t mean everything though, Millicom has the highest growth in revenues, and Orascom has the highest EBITDA margin, primarily due to its strategy of investing in the emerging mobile markets.

The chart below shows five of the leading mobile network operators in Africa in terms of their subscriber base (size of the bubble), revenue growth rate and EBITDA margin for the latest completed financial year.

In Summary

The growth rate in Africa over the last couple of years has been phenomenal, and will likely continue for the next 3-5 years. Major drivers of increased growth include:

- Subsidization of handsets

- Pre-paid offerings

- Continued liberalization of the telcom sector

- Low penetration rates

- Expected uptake of 3G services

Growth inhibitors include:

- Taxation – especially in East Africa

- Low income across the continent hampers growth

- Widespread illiteracy decreases the growth of value added services, even SMS

- Unreliable electricity supplies

- Corruption

I’m curious to see the uptake of both data services (3G and EDGE) as well as the increased number of low-cost handsets. Just yesterday I read a report of a Malaysian company setting up a mobile phone manufacturing plant in Mozambique, so there very well might be some super low-end phones available soon.

]]>