I’ve argued before, alongside others, that the main inhibitor of ubiquitous and perpetual internet connectivity at a global level isn’t a technology problem, it’s a business model problem. Mostly the tech exists to put the signal everywhere. What we overlook when we say this is, that while that is true, it’s unsavory to point out that many of “those users” are not valuable – that the population covered won’t make a good return on business investment. So, even if you covered the initial cost of the equipment outlay in those areas with a subsidized government funds, without a proper business model to support the ongoing operations of running the network, then the ROI would be weak and maybe even negative.

A low cost tower set up in rural Africa

The unspoken technology issue

Many of the incumbent ISPs and mobile operators have sunk too many resources into legacy technology, and then subsequently, outsourced their technical capacity and platform knowledge to foreign firms. This leaves them in an unfavorable position when it comes to new technology that would decrease the cost of rollout by up to 90%, or of taking advantage of how software is changing the way networks work. Due to heavy GSM investment, the industry thinks it best to switch those from 2G/EGDE to 3G. This misses the mark though, it’s iterative change driven by sunk costs, ignoring the fact that we’re moving to a data-only network world. GSM is a dead man walking. IP networks are the future.

It’s not just me saying this, two years ago Deloitte was saying,

“African MNOs should create business models around smartphone users and brace for the rise of the data exclusives and data centric phone users.”

This then provides the opportunity. This is the time to bring new networks without legacy business or technology paradigms, and the ability to apply web-scale economics to the network itself, backstopped by new open software stacks and business models that don’t rely solely on end-user payment.

Fortunately at BRCK we’ve been able to find great investors and strategic partners who see this bigger picture and understand the investments needed to make change happen in this connectivity industry of ours. BRCK, alongside some other firms, are on the forefront of changes happening across all types of data pipes, at the infrastructure level all the way through to the retail side – for both people and things. And as we start running the numbers it becomes increasingly clear just how big of an opportunity this actually represents. It only helps that many incumbents are stuck in aged technology stacks and legacy business models, so the window for positive change is here and profits are substantial.

East Africa Railways train

A new railroad

I tend to think of what we do in the connectivity space as similar to our forebears building railroads, making it easier, faster and more efficient to move data and connect far-flung parts of the world. The 1990’s brought us the rebels in the form of scrappy upstart mobile operators and ISPs, they were real cowboys and renegades then! Inspiring leaders, courageously trying everything from pre-paid credit models in Africa, to thinking of mobile credit as cash, to digging the first fibre cables into the hard parts of the continent. Regrettably, these cowboys have handed the reins over to our modern day robber barons, sitting fat and happy on their oligopolies (or monopolies), and making damn sure that no one else has a chance to build something better if they can help it.

I like to think that at BRCK we are building the new connectivity railroads. The tip of the spear for us is unlicensed spectrum, where we take advantage of the ability to roll out public WiFi hotspots without much in the way of regulatory or political hurdles. We layer this with a free consumer business model, so that anyone who can get that signal can connect and take advantage of the whole internet. The underlying economics of the Moja platform are built around the idea of a digital economy. Businesses create engagement tasks that users can complete to earn value within the system. Users then spend their value on faster connectivity, premium content, or additional services. The flow of value into and out of the Moja platform creates the monetary value necessary to profitably run the network.

This is just the BRCK model though, and as I sit on some global boards and in meetings I hear of the others trying their new models as well. New technology stacks, driven primarily by open source software (and some key open source hardware plays), are a big part of the significant decrease in the cost profile (both CapEx and OpEx). But again, the business models… this is where we see the real changes coming and I’m excited to have a front row seat.

As these new railroads are built, by us and others, there lies such great opportunity for economic growth, social development, and business profit.

Sponsor this article: casino cashlib and casino en ligne yggdrasil

]]>Send me any that I might have missed.

Early stage capital

Angani – Public cloud computing provider

BRCK – Rugged, wireless WiFi device

CardPlanet – Mobile money payment system aimed at business and NGOs

iProcure – Software for optimizing rural supply chains

OkHi – Physical addressing system for logistics solutions

Sendy – Motorcycle delivery service

Tumakaro – Diaspora driven education funding

Umati Capital – Factoring for farmer cooperatives, traders and processors

GoFinance – Working capital finance to distributors of FMCGs

BuyMore – Electronic student discount card

TotoHealth – SMS technology for children’s health

BitPesa – Bitcoin for African remittances

Sokonect – Mobile agriculture tool to eliminate brokers

BookNow – Buy bus tickets online in East Africa

Mdundo – African music on your phone

Futaa – Source for football news in Kenya

Movas – Global provider of B2B/B2C m-Commerce solutions

Hivisasa – A free, county-level online newspaper

Yum – Online ordering and food delivery service in Kenya

Akengo – Learning management system

EcoZoom – Hardware. Clean burning, portable wood and charcoal powered cookstoves

Jooist – A gaming network for mobile phones

Globa.li – A platform to connect hotels and distributors for bookings

Growth capital

MKopa – solar power financing using mobile money

BuyRentKenya – Real estate classifieds

Wave – US-to-Kenya remittance provider

Eneza Education – Mobile tutor and teacher’s assistant

Sanergy – hardware tech, building solutions for urban toilets and composting

Bridge International – Education in low-income environments, uses tech to send teaching content

Soko – Handmade jewelry and accessories shopping from East Africa

EatOut – Find and book seats in East African restaurants

Exited/Acquired

M-Ledger (by Safaricom) – Monitor your Mpesa transactions

Wezatele – Mobility solutions in commerce, supply chain, distribution and mobile payment integration

A special thanks to John Kieti, Rebecca Wanjiku, Nikolai Barnwell, and Ben Lyon for refreshing my memory!

]]>It’s 6am in Lusaka, Zambia as I write this. The last two days have been a blur as we covered over 1,700 kilometers from Dodoma to Lusaka in what can only be considered as marathon sessions from sunup to just after sundown. Fortunately, both Tanzania and Zambia have some of the best roads we’ve seen, and the motorcycles and car all behaved well with only one slow puncture the whole way. We took small breaks every 100-200km in order to rest and move around a bit, but we’re still quite sore and ready for this day to do no travel.

Parking lot mechanics in Dodoma, Tanzania

Mark, Juliana and Joel setting up the GoPro

A dawn stop on the way out of Dodoma to Iringa, Tanzania

Grabbing lunch somewhere in southern Tanzania

The border crossing from Tanzania into Zambia at Dunduma left a little something to be desired. What felt like it should have taken about 1.5 hours at most, ended up taking 3+ hours, which meant our last 50km into a campsite were done in the dark on the only section of bad road we’ve seen. People did warn us of this, so it wasn’t unexpected. However, the reason wasn’t because of long lines of trucks slowing us down, it was due to inefficiency in the process itself at both immigration and customs.

From here, our days get a little more sane, with a run down through Victoria Falls into Botswana and then finally Johannesburg. As an aside, it turns out that half-way between Nairobi and Jo’burg is almost exactly at a small town called Serenje, Zambia – 2,200km from each.

Time at Bongohive

We pushed so hard to get to Lusaka by now so that we would be here in time for the events at Bongohive, Lusaka’s tech hub, which were all scheduled for today.

1pm – Demo of BRCK (Philip Walton and Reg Orton of the BRCK team)

3pm – Meeting with Startups (Mark Kamauof the iHub UX Lab) – HCD, UX, DT

4:30pm – Meeting with Startups (Erik) – Investment readiness, experiences with Savannah Fund, getting into new markets etc

6pm – Keynote at Startup Weekend Lusaka (Erik and Juliana Rotich)

Lukongo Lindunda is the co-founder of the space, and we’ve known each other for years, since before they got it started back in 2011. I’ve been looking forward to seeing everyone here in the tech space for a while, and I’m interested in hearing what’s brewing in the startup scene.

Some of the startups that I’ve heard about from Zambia include:

- ShopZed.com

- Bantu Babel

- Venivi

- DotCom Zambia, BusTickets

- TeleDoctor

- SCND Genesis

If you’re part of the tech community in Zambia, I hope you can swing by, and we’re all looking forward to seeing you as well.

Lessons From the Trip

Since we’ve started this trip I’ve been thinking a lot about communications, as one would expect with a BRCK expedition, and especially mobile comms. We outfitted the truck with a omni-directional Poynting antenna on the front bumper, hooked up into the car, where we can also connect it to an amplifier if needed. As we drive down the road, we have a pretty good mobile WiFi hotspot, as long as we’re in range of a tower.

The mobile phone kiosk, a mainstay of rural Africa

The last few years have seen a number of countries implement a registration process to buy SIM cards (ostensibly this is for security though it’s not been proven to be useful for anything more than big brother activities by governments). Even buying a SIM card is then a process of identification (usually passport or drivers license), so you have to budget for that 30-60 minutes to get that done, since it’s usually filling out a form by hand.

Registering an MTN SIM card in Zambia

You then purchase credit for the SIM card and load it up – this is the easiest part.

Now you get into the “mystery meat” part of the process, which is how do you turn that airtime you just bought into internet credit? Each network in each country has a different way of doing this, some combination of USSD or SMS to get it going.

A couple things come to mind now when we look at the BRCK.

First, we need a terminal screen in the BRCK interface for us to do all of this from the device itself. Right now we find ourselves popping out the SIM card and using a phone (Mozilla’s 3-SIM phone is amazing for this purpose), and then inserting it back into the BRCK when done.

Second, there needs to be a database of this “airtime to internet data” information that we can all use. I’m not sure how best to get this going, but I know it would be immensely useful when you drop into a new country to have this at your fingertips.

We’re already working on the first issue, of USSD/SMS interface, but it’s complicated, so it’s taking longer than we’d like. This trip is about learning, and we’re already finding a lot of things to do better. Look for more posts on the BRCK blog from the others as well.

]]>1. The Akamai “State of the Internet” Q3 2013 report

[Akamai Report – PDF Download]

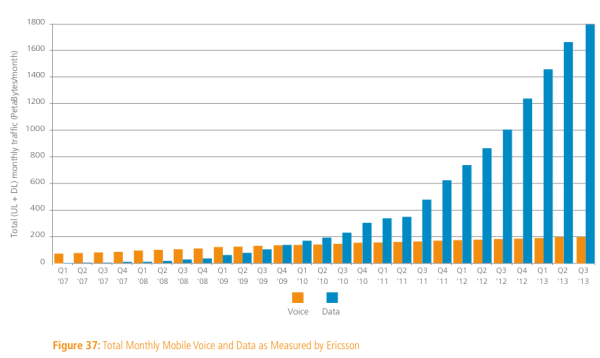

Has good information on overall usage globally, and trends. In Africa, even though they have a node in Kenya, all we’re seeing is stats on South Africa, Egypt and Morocco. However, there is a really fascinating chart by Ericsson in it on wireless usage.

Mobile data vs voice growth globally – 2013

2. GSMA’s “Digital Entrepreneurship in Kenya” report 2014

[GSMA – Entrepreneurship in Kenya report 2014 – PDF Download]

The GSMA puts together some fantastic reports, due to the amount of data at their fingertips due to their association’s membership. Alongside the iHub Research team, they’ve done a deep dive into the tech entrepreneurship side of Kenya, and you can see the results here.

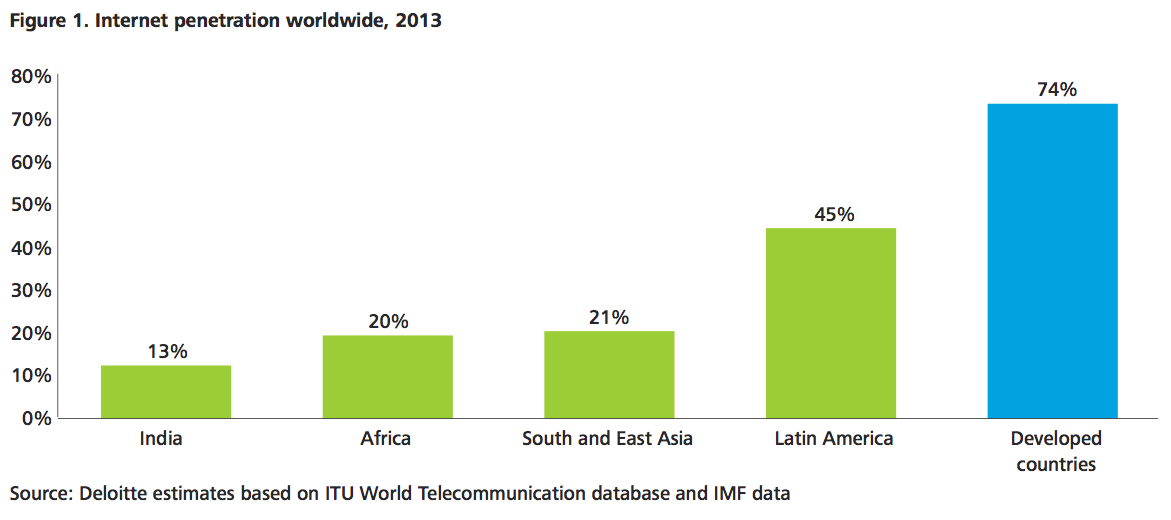

3. Deloitte’s “Value of connectivity” report 2014

[Deloitte’s – Extending Internet Connectivity report 2014 – PDF Download]

The Deloitte folks do a study and argue that an increase in internet penetration could have a large impact on an emerging market country’s GDP.

“Deloitte estimates that the resulting economic activity could generate $2.2 trillion in additional GDP, a 72% increase in the GDP growth rate, and more than 140 million new jobs.”

4. infoDev’s “The Business Models of mLabs and mHubs” report 2014

[The Business Models of mLabs and mHubs 2014 – PDF Download]

I’ve had a front-row seat to infoDev’s work starting and supporting places like the m:lab in East Africa. After doing it for 3 years, here’s their indepth report on what’s working, not working, how much money has been spent and what the future might look like.

5. McKinsey’s “The Internet’s transformative potential in Africa” report 2013

[MGI Lions go digital_Full report_Nov 2013 – PDF Download]

Mostly useful due to the interest large corporates and banks put in McKinsey, this report makes that the greatest impact of the internet in Africa is likely to be concentrated in six sectors: financial services, education, health, retail, agriculture, and government. What they’ve done particularly well is gather a large range of numbers from diverse and various sources to make better sense of what’s going on.

he iHub started in March 2010, so it’s been about 3.5 years and a lot has happened here in the intervening years. Many people ask me, “so, what has the iHub done?” The best way I could think of to answer that is to just list as much as I could think of, so here’s a rather exhaustive list, though I’m sure that I’m missing some things.

Why Tech Hubs in Africa Exist

Nairobi tech community working at the iHub, circa 2011

Before I get into that though, maybe a framing on why tech hubs exist is important. They’re not just there for startups, in fact our thoughts on incubation and products going back to 2010 was just pre-incubation and connecting to other businesses and investors. Places like the iHub exist to connect this community together, while we get involved in other gaps that exist in the market (UX, incubation, research, etc), these are just part of providing a place where serendipity happens for those who are involved across the network.

These spaces are more than just nurturing talented entrepreneurs, and to not see that means you’re missing the bigger picture on why they exist. They’re not only about entrepreneurs, though we have seen some of them grow from nothing to 40-person orgs that run across multiple countries.

The tech hubs in Africa are more than just places focused on products, much of what goes on is about connecting the people within the tech community in that area to each other and to the greater global industry. For instance, we started Pivot in East Africa, an annual event that does two things: First, it created a culture where the entrepreneurs learned how to pitch their products. Second, it gave a reason for local and global investors and media to come and see what’s going on. Both funding and media coverage have resulted.

Another example is the connecting of global tech companies to local developers, the training that comes out of it for everyone from network operators to Android devs. Google, Samsung and Intel all play strongly in that space.

Some work at increasing the viability and skillsets of freelancers. Whether they’re web designers or PHP software engineers increasing their understanding of how to setup a company, know what IP law is about, take training on project management or quality assurance testing – these all add up to a community that is evolving and becoming more professional.

Those are just a few of the things that tech hubs do across Africa. I can speak for the iHub in Kenya, but know that there are others such as ccHub in Nigeria, Banta Labs in Senegal, ActivSpaces in Cameroon and the other 19 tech hubs in the Afrilabs network are all doing amazing things that create a base for new innovative products, services and models to grow out of. There are new models for ecosystem development around tech in Africa revolving around these technology hubs that are, and will breed, more innovation over time.

New initiatives and organizations from the iHub:

m:lab – first tech incubator in Kenya (2011)

Mobile testing room – all the tablets and phones from the manufacturers (2011)

iHub Research – tech focused research arm (2011)

UX Lab – first user experience lab in East Africa (2012)

iHub Consulting – an effort to connect freelancers to training and businesses (2012)

Savannah Fund – a funding and accelerator program (2012)

Cluster – first open supercomputer cluster in East Africa (2013)

Gearbox – an open makerspace for rapid prototyping (2013)

Code FC – iHub Football Club

Volunteer Network team – the iHub internet network was setup, and is run by, volunteers

Startups who met, work, or started in the iHub:

BitYarn

NikoHapa

KopoKopo

M-Farm

BRCK

Eneza Education

Ma3Route

Uhasibu

Fomobi

Whive

Zege Technologies

Afroes Games

iDaktari

MedAfrica

SleepOut

M-shop

Angani.co

Wezatele

AkiraChix

Upstart Africa

Juakali

CrowdPesa

Elimu

iCow

Sprint Interactive

Lipisha

6 Degrees / The Phone book

Pesatalk

Skoobox

Waabeh

MamaTele

RevWebolution

Smart Blackboard – Mukeli Mobile

Not all groups start their company at the iHub, but they do meet their future business partners there. The Rupu founders met at an iHub event, and subsequently went on to grow their business, the same is true of companies like Skyline Design, and probably many others who we don’t even know about.

It turns out that serendipity is intrinsically hard to measure.

Larger events, groups and meetings:

One of the 120+ events that takes place at the iHub each year.

- Pivot East – annual pitching competition for East Africa’s mobile startups

- iHub Robotics (now Gearbox community) meet-ups and build nights

- EANOG – East Africa Network Operators Group

- Kids Hacker Camp – 40 kids hack on Arduino, learn about robotics and sensors in a week long full-day hackathon, in partnership with IBM

- NRBuzz – A monthly event on sharing research on new technologies and communication

- Summer Data Jam – an annual 6-weeks training on Research and Data

- Tajriba – month-long user experience event

- m:lab mobile training – 22 students, 4 months, business and mobile programming (2 years to date)

- Legal month – annual event with visiting legal professionals leading workshops

- Barcamp Nairobi (2010, 2011, 2013)

- Waza Experience – volunteer outreach initiative to expose Kenyan youth to technology and spur creative thinking, problem solving, and better communication skills

- Fireside Chats – A session for VIP and seasoned speakers

- Mobile Monday

- Wireless Wednesday

- JumpStart Series

- Pitch Night

- iHub Livewire – music concert by the iHub community

- iHub Research Coffee Hour

- We have a Policy Formulation Team which consists of Jessica Musila, Martin Obuya Paul Muchene, and Jimmy Gitonga. Each one of us sits or has sat through a policy formulation process, such as the AU CyberSecurity (Martin and Paul) and MySociety, Mzalendo (Jessica Musila) and National Broadband Strategy (Jimmy Gitonga).

Outreach events

Egerton University

Catholic University

Kabarak University (Nakuru)

JKUAT (Juja)

Dedan Kimathi (Nyeri)

Maseno University

Nelson Mandela University – Arusha

Strathmore / Intel

University of Nairobi – School of Computing and Informatics

Research-related activities:

Launching of the Data Science and Visualization Lab – 2013

First Summer Data Jam Training – 2013

Research published:

- Digital libraries and crowdsourcing – http://bit.ly/1boQpeI

- The Gap Between Mobile Application Developers and Poor Consumers: Lessons from Kenya. Proceedings of CPRsouth8. September 2013.

- 3Vs Framework for Crowdsourcing. August 2013.

- Umati Final Report June 2013.

- Umati: Kenyan Online Discourse to Catalyze and Counter Violence. IFIP 2013 Conference Proceedings. May 2013.

- Startup Business Models and Challenges for East African mAgriculture Innovations. IST 2013 Conference Proceedings.

- Mobile Phone Usage at the Base of the Pyramid in Kenya. InfoDev World Bank. December 2012.

- M-governance: Exploratory Survey on Kenyan Service Delivery and Government Interaction. IST 2012 Conference Proceedings.

- Increasing Kenya Open Data Consumption: A Design Thinking Approach. Proceedings of ICEGov 2012.

- Meshcasting News in the Port Harcourt Waterfronts. Internews. May 2012.

- Development of Local Educational Digital Content For Schools In Kenya Using The Mobile Device As An Acceleration Tool To Enhance Learning And Facilitate Collaborative Learning

- Growth Of Mobile Education Platforms And The Impact On Learning In Primary Schools In Kenya

List of infographics created (PDF Links):

Mobile Technology in Tanzania: 2011

Mobile Technology in Uganda: 2010/2011

Mobile Technology in Kenya: 2010/2011

Kenya Open Data Pre-Incubator Plan: 2012

3Vs Crowdsourcing Framework for Elections: Using online and mobile technology: 2013

How to Develop Research Findings into Solutions using Design Thinking: 2013

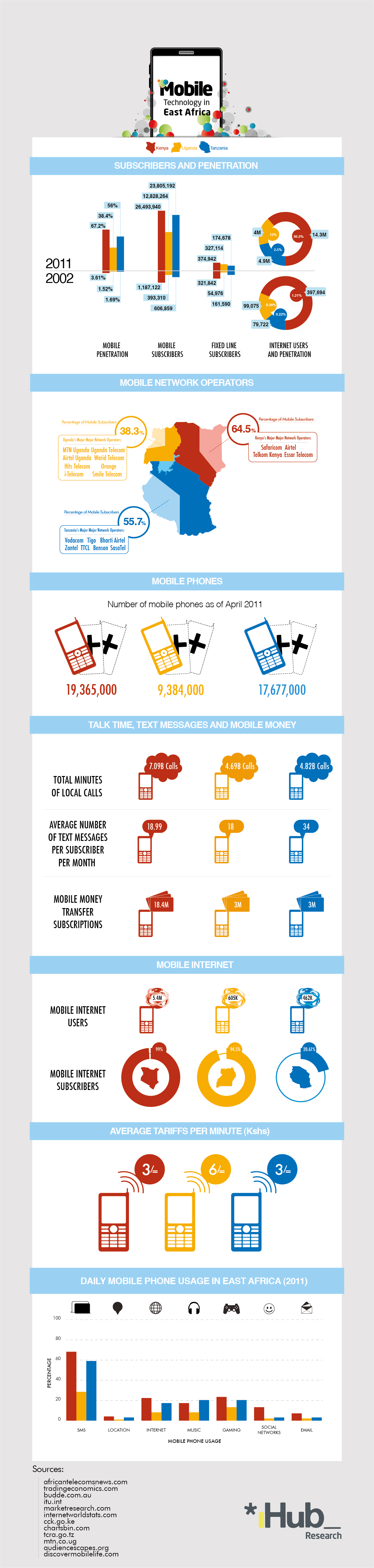

Mobile Statistics in East Africa: 2013

iHub Infographic: 2011

Crowdmap Use

Mobile Tech in East Africa: 2011

An Exploratory Study on Kenyan Consumer Ordering Habits

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tech hubs in Africa research (PDF Links):

ICT Hubs Model: Understanding the Factors that make up Hive Colab in Uganda: August 2012

ICT Hubs Model: Understanding the Factor that make up ActivSpaces Model in Cameroon: August 2012

The Impact of ActivSpaces model (in Cameroon) on its Entrepreneurs: January 2013

Draft Report on Comparative Study on Innovation Hubs Across Africa: May 2013

ICT Hubs model: Understanding the Key Factors of the iHub Model, Nairobi Kenya: April 2013

ICT Hubs model: Understanding Factors that make up the KLab Model in Rwanda: April 2013

ICT Hubs model: Understanding Factors that make up the MEST ICT Hub – ACCRA, Ghana: April 2013

ICT Hubs model: Understanding Factors That Make Up Bongo Hive, Lusaka Zambia: April 2013

ICT Hubs model: Understanding Factors that make up Kinu Hub Model in Dar es salaam, Tanzania: April 2013

Key partnerships:

- Intel

- Wananchi Group – ZUKU

- SEACOM

- Samsung

- Microsoft

- Nokia

- Qualcomm

- MIH

- InMobi

VIP speakers:

- Michael Joseph, Safaricom

- Joseph Mucheru, Google

- Vint Cerf, Google

- Stephen Elop, Nokia

- Marissa Mayer, Yahoo

- Bob Collymore, Safaricom

- Larry Wall, Creator of Perl

- John Waibochi, Virtual City

- Mike Macharia, Seven Seas

- Ken Oyola, Nokia

- Isis Ny’ongo, Inmobi, Investor

- The tweeting Chief Kariuki

- Louis Otieno, Microsoft

- Dadi Perlmutter, Intel

- Susan Dray, Dray and Associates

The full Ushahidi team met yesterday (many virtually, of course), and we talked about many issues surrounding the Westgate siege. Not least amongst them was the fact that we had a hard time checking in with each other. And then found out that one of our team’s wife and 5 children were inside of the mall, while he was traveling out of country. They eventually got out a few hours later, to which we were relieved.

This lead us to then think through our skills and tools, and where we could be useful.

In an emergency, how do you find out quickly whether your family, your team, your friends are safe?

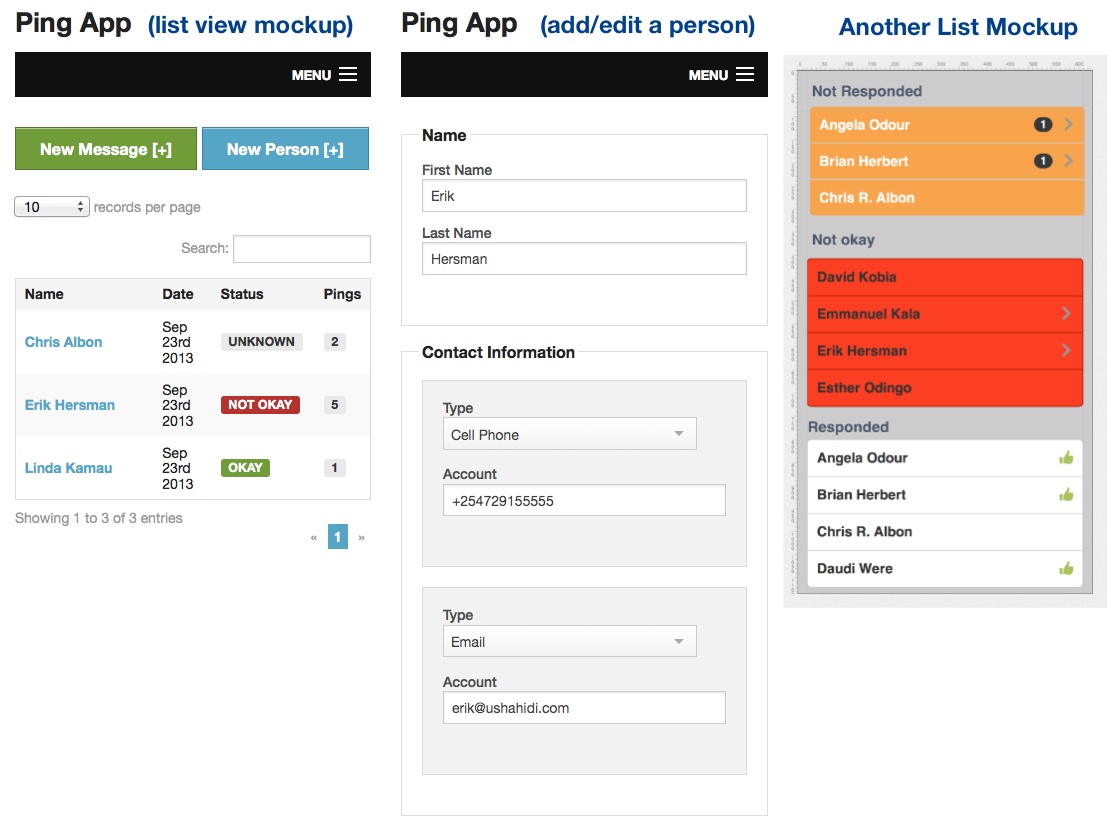

The Ping App – a group check-in tool for emergencies

How About a Way to “Ping” Your Group?

There was a consistent problem in every disaster that happens, not just in Kenya, but everywhere. Small groups, families and companies need to quickly check in with each other. They need to “ping” one another to make sure they’re okay. It has to be something incredibly simple, that requires little thinking to use. People have been doing some stuff in this space in the past, the best like “I’m Ok” are focused on smartphone users, but we have a need to make it work for even the simplest phones. Our goal is to have this available for anyone globally to use.

“Ping” is basically a binary, multichannel check-in tool for groups. The idea is that families and organizations could use this for quick headcounts on how everyone was, then use it as an on-ramp into a Red Cross missing persons index or something like Google’s People Finder app.

We’re putting the first version of it up at Ping.Ushahidi.com – here’s how it works:

- You create a list of your people (family, organization), and each person also adds another contact who is close to them (spouse, roommate, boy/girlfriend, etc).

- When a disaster happens, you send out a message for everyone to check-in. The admin sends out a 120 character message that always has “are you ok?” appended to the end.

- This goes out via text message and email (more channels can be added later).

- The message goes out three times, once every 5 minutes. If there is a response, then that person is considered okay. If no response, then 3 messages get sent to their other contact.

- We file each response into one of 3 areas: responded (verified), not responded, not okay.

- Every message that comes back from someone in that group is saved into a big bucket of text, that the admin can add notes to if needed.

Ping Notes, Features

Ping Architecture – rough draft

Yesterday we quickly wireframed out a list of needs, some design basics, and an architecture plan (images above), got a rough product going on it (code is on Github). We now need to make it look better, so some designers are working up some stuff to make it work well on both phones and computers.

Mockups of the Ping app, still undergoing some design tweeks

Final touches are to add in:

- Account creation, we’re using our CrowdmapID tool for this, since it’s already out

- Message “send” page

- Archive old campaigns feature

- Wire into text messaging service (Nexmo or Twilio), and then testing it out internally

- Designing it so it looks good (responsive design, so it works on mobiles and PCs)

If you’d like to help out, jump on the Github repo, and get in touch with us about what you can do. What we have here is a minimum viable product (MVP) right now, open source, so anyone can make it better by branching the code and adding in features, etc.

Finally, a HUGE thank you to the people who have been burning the midnight oil to make this all happen in 24 hours:

@udezekene (visiting from Nigeria)

@EmiliaMaj (visiting from Poland)

@gr2m (visiting from Germany)

@Dkobia (Ushahidi)

@LKamau (Ushahidi)

@bytebandit (Ushahidi)

@DigitalAfrican (Ushahidi)

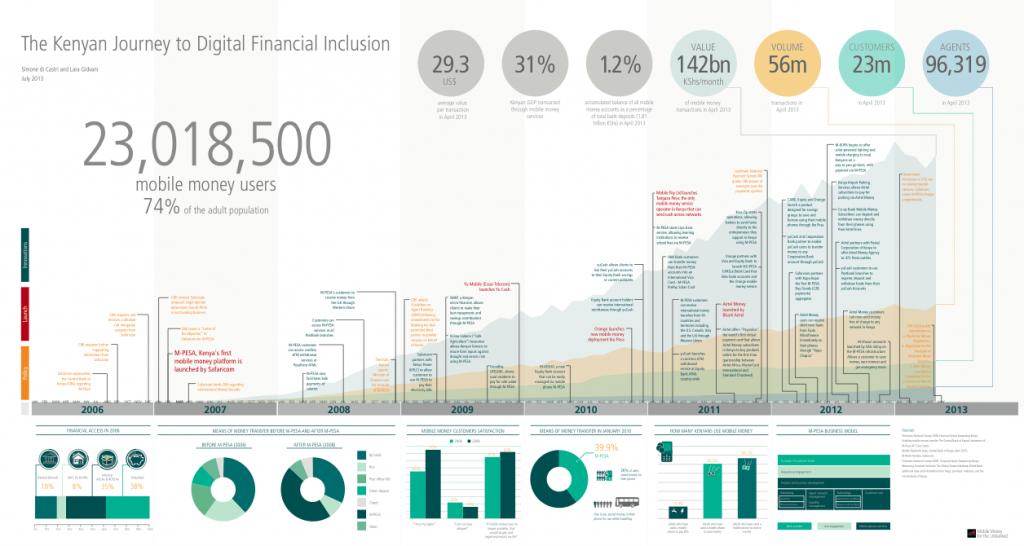

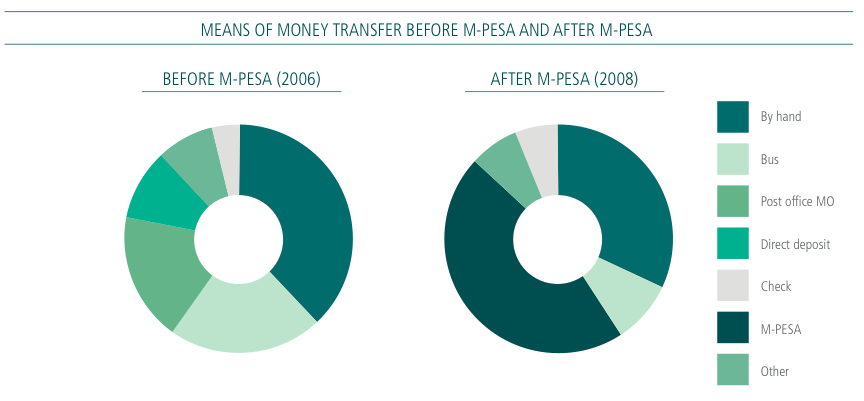

A Kenya mobile money infographic (2013) by the GSMA

Interesting figures for 2013:

Average value per transaction: $29

Percentage of GDP transacted: 31%

By April 2013 Mpesa:

- Averages 142bn Ksh transacted per month. ($1.67 billion)

- Has a total of 56 million transactions per month

- Has 23 million customers

- Has 96,000 agents around the country

Also in 2013, the Kenya government levies a flat tax of 10% on all Mpesa transactions. Safaricom also raises charges to counter this. All users now pay more, but it’s hidden so that you don’t see the charge, unless you do the math on the balance remaining after you send funds.

Means of money transfer before and after Mpesa

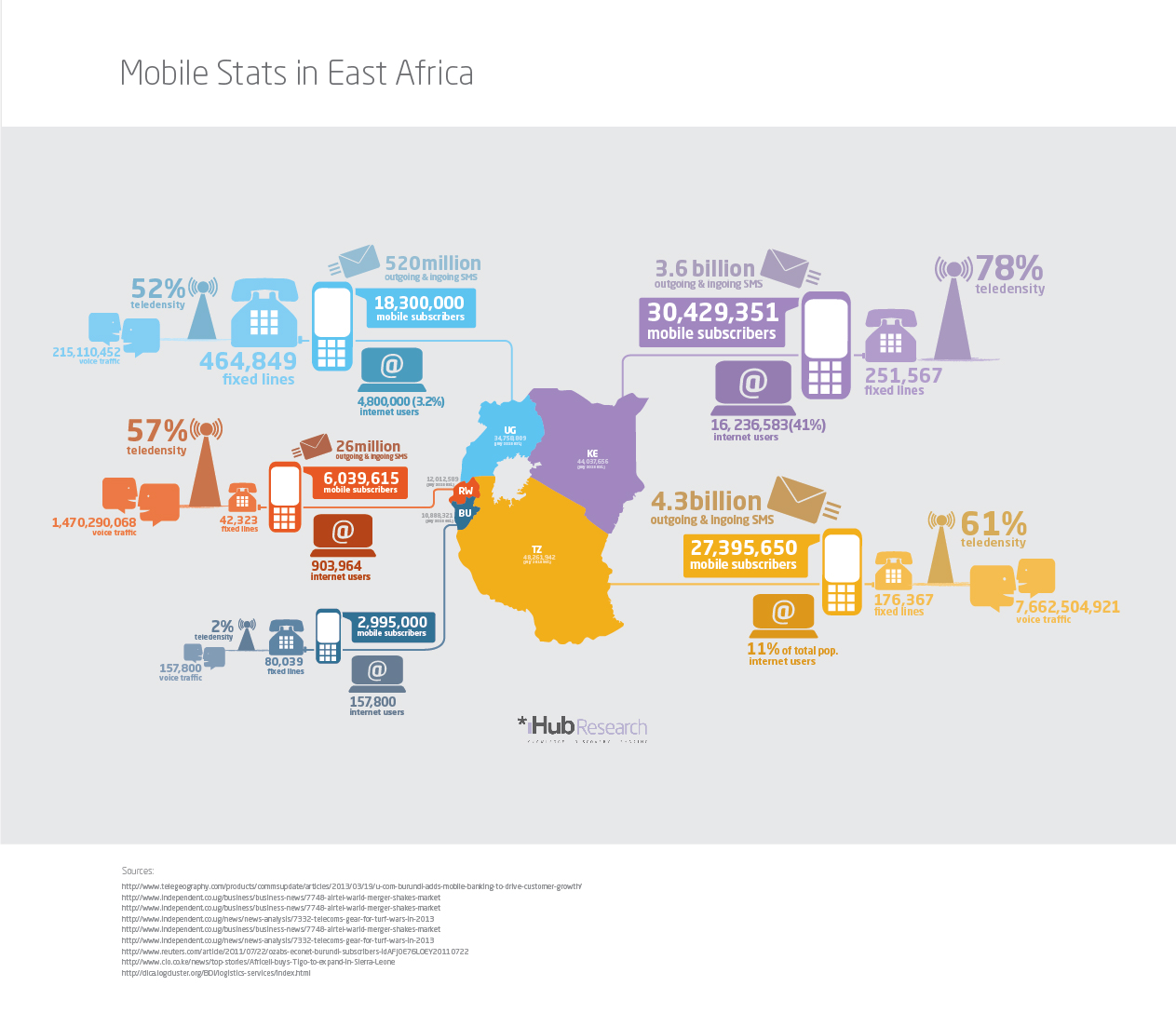

Mobile & Internet Stats for East Africa

The most recent stats for East Africa’s mobile and internet usage have been put into an new infographic.

Mobile and Internet use in East Africa, an infographic by iHub Research

Here is a dump of the data used for this infographic:

Kenya Mobile Statistics

(Population: 44,037,656 July 2013 estimate)

30,429,351 mobile subscribers

16,236,583 (41%) Internet users

3.6 billion outgoing & incoming SMS

251,567 fixed lines

78% teledensity

Tanzania Mobile Statistics

(Population: 48,261,942 July 2013 estimate)

27,395,650 mobile subscribers

5,308,814(11%) Internet users

4.3 billion outgoing & incoming SMS

176,367 fixed lines

61% teledensity

7,662,504,921 voice traffic

Uganda Mobile Statistics

(Population: 34,758,809 July 2013 estimate)

18,300,000 mobile subscribers

4,800,000 (3.2%) Internet users

520 million outgoing & incoming SMS

464,849 fixed lines

52% teledensity

215,110,452 voice traffic

Rwanda Mobile Statistics

(Population: 12,012,589 July 2013 estimate)

6,039,615 mobile subscribers

903,964 Internet users

26 million outgoing & incoming SMS

42,323 fixed lines

57% teledensity

1,470,290,068 voice traffic

Burundi Mobile Statistics

(Population: 10,888,321 July 2013 estimate)

2,995,000 mobile subscribers

157,800 Internet users

80,039 fixed lines

2% teledensity

157,800 voice traffic

Sources:

http://www.telegeography.com/products/commsupdate/articles/2013/03/19/u-com-burundi-adds-mobile-banking-to-drive-customer-growth/

http://www.independent.co.ug/business/business-news/7748-airtel-warid-merger-shakes-market

http://www.independent.co.ug/news/news-analysis/7332-telecoms-gear-for-turf-wars-in-2013

http://www.independent.co.ug/business/business-news/7748-airtel-warid-merger-shakes-market

http://www.reuters.com/article/2011/07/22/ozabs-econet-burundi-subscribers-idAFJOE76L0EY20110722

http://www.cio.co.ke/news/top-stories/Africell-buys-Tigo-to-expand-in-Sierra-Leone

http://dlca.logcluster.org/BDI/logistics-services/index.html

CIA World Factbook

2011/2012 Stats and Infographic

Here’s the 2011/2012 numbers for all of the countries in East Africa, plus some bonus numbers around mobile money at that time.

{kind=link}

2011 and 2012 East Africa mobile and internet statistics infographic by iHub Research

See the old ones from 2011 in Uganda, Kenya and Tanzania. You can also see the some 2012 numbers on the iHub that they put together as well.

]]>(This is my daughter at Lake Naivasha at sunrise)

Enough people have asked me about how I Instagram that I thought it might be worth creating a post on it. I take a lot of pictures as I travel as it gives me something to do along the way, so there are a lot of pictures in my stream from all over the world. I’m a hobbyist, with no pretensions of being a pro.

You can find me at @White_African on Instagram.

I’m starting a tag game with this, now hitting @Truthslinger with #HowIInstagram to see how he does it.

Hardware

iPhone only (I’m on an iPhone 5 these days). I’d guess that 80% of my shots are taken with just the camera and no extra hardware. However, sometimes I mod it with the following items.

These are the hardware mods that I use for iPhone Instagramming: Olloclip + Lifeproof + Joby

An Olloclip lens ($70): which gives me a wide-angle, fisheye and macro-lens all in a small form that I can fit in my pocket. It’s fantastic. Here are 3 examples of it.

Underwater Lifeproof case: I don’t have this on all the time, only when I’m specifically going out for underwater or am in a boat taking crazy angle shots. Another great add-on that let’s you take some cool shots.

Joby GripTight Microstand (Tripod) ($30): I hardly ever use it, but when taking some macro pictures it comes in very useful as I just can’t hold my hand steady enough to get the shot.

Something I’d like to get is a good telephoto lens for the iPhone.

Software

Camera+ ($1.99): This is my most basic quick-edit app, since I can do multiple shots quickly and it does a good job with clarity and quick filters. I tend to tone down most of the filter choices.

Snapseed (free): When I really want to edit an image, a special one that needs a lot of extra attention to detail, I use Snapseed. If you’re an Android user, they have it for you as well.

ProHDR ($1.99): I like color, so to really make colors pop I’ll use an ProHDR to do it properly. A lot of good in-app controls. My favorite picture from last year was taken with it:

(A tree in a park in Camden, Maine during the Fall)

Over ($1.99): If you like to put text over your images, there is no better iPhone app for it than Over. Many awards and also made by my friend @AaronMarshall.

Other apps that I use either randomly or rarely:

- NoIMGdata ($0.99): wipe all the sensitive EXIF data from the picture for privacy

- SlowShutter ($0.99): a great app for light trails or low light

- Reduce ($1.99): for when the image size needs to be smaller

10 of my favorite shots

(Boats near the harbor in Camden, Maine)

(Making sun tea in Diani, Kenya coast)

(A quiet pool and shady trees in rural England)

(At Yale University, USA)

(Mark and Tosh relaxing on Diani Beach, Kenya)

(The iHub team at Diani Beach, Kenya)

(Satellite, the only way to get internet at a ranch near Tsavo, Kenya)

(Emmanuel doing a summersault off a dhow near Lamu, Kenya)

(Olloclip macro lens on a burning candle)

(Jumpshot at Strathmore high school, Kenya)

The Kenya365 Project

In September 2012, we started a #Kenya365 project for anyone in Kenya to take a picture a day and tag it with that hashtag. The amazing @Truthslinger runs it, and we have weekly themes that he sets up. Take a look to see some great shots from around Kenya, and join in. The only rule is that you can only tag one picture per day with #Kenya365 on it.

]]>

The main office for the GSMA is in London, and their times in Nairobi coincided with their internal strategy discussions on opening up offices in each continent. Today they are opening up their Africa office, which is on the first floor of the iHub building (Bishop Magua Centre), on Ngong Road.

This is great news for all parties, as it brings the large mobiel operators into closer connection with the startups and tech innovators found in the building already, and it allows the tech companies to better connect to the association that bridges the big mobile players. I’m excited about what will come from the interactions that this new space will bring.

My experiences with the GSMA team, both in Kenya and London, have left me with nothing but a great amount of respect for what they’re doing globally. I also love them for their mobile statistics and reports, which is why I’ll leave some exerpts from their press release here:

Why the office in Nairobi?

“The rapid increase of mobile connections has attracted GSMA to the region. Mobile connections in Sub-Saharan Africa increased by 20 per cent to 500 million in 2013 and are expected to increase by an additional 50 per cent by 2018. The GSMA’s permanent presence in Kenya will enable the organisation to work closely with its members to put the conditions in place that will facilitate the expansion of mobile, bringing important connectivity and services to all in the region.”

From their Anne Bouverot, Director General, GSMA:

“The rapid pace of mobile adoption has delivered an explosion of innovation and huge economic benefits in the region, directly contributing US$ 32 billion to the Sub-Saharan African economy, or 4.4 per cent of GDP. With necessary spectrum allocations and transparent regulation, the mobile industry could also fuel the creation of 14.9 million new jobs in the region between 2015 and 2020.”

On the internet and data:

“In Zimbabwe and Nigeria, mobile accounts for over half of all web traffic at 58.1 per cent and 57.9 per cent respectively, compared to a 10 per cent global average. 3G penetration levels are forecast to reach a quarter of the population in Sub-Saharan Africa by 2017 (from six per cent in 2012) as the use of mobile-specific services develops.”

You can read the full press release here.

]]>